Introduction

Current Market Conditions

2024 Market

-

Fannie Mae economists say they expect only 4.01M existing homes to change hands this year – which would make 2024 the slowest year for national home sales since 1995.

-

High demand and low inventory continued to define the Daniel Island Real Estate market in 2024.

-

Closed sales on DI lowered -8% from 2023, but the median sales price increased +7.4% (CTAR MLS).

-

Average sales price for DI increased +18.7% due to strong upper price-point sales (above $5M). (CTAR MLS)

-

Inventory of Homes for Sale was held low by owners’ desire to hold their current low interest mortgages instead of trading them for new mortgages with higher rates (i.e. the “Golden Handcuffs”).

-

The market’s perception of interest rates remain high – at current rate of 6.84%.

-

For homes sold in 2024 the final sales price was a median of 100% of the final listing price. This is the highest recorded median since 2002. Seller’s market! (NAR)

-

+40% of Sales in this market are all-cash.

2024 Buyers

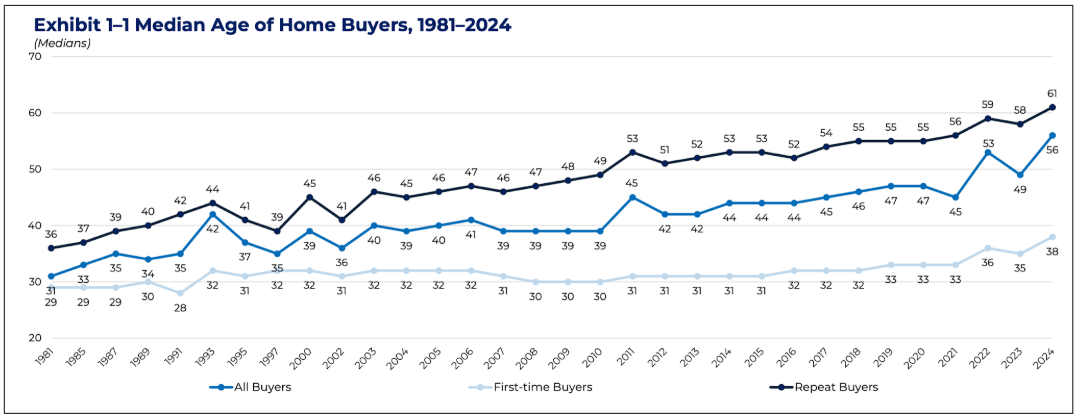

- The ages of home buyers reached all-time highs. The median repeat buyers age increased to 61 years old.

- The median first-time buyer age increased to 38 years old.

- 73% of recent buyers did not have a child under 18 in their home – the highest share ever recorded.

- First-time home buyers decreased to 24% - the lowest share since 1981. 66% of home buyers stated that their decision to buy had little to do with the real estate market or availability of homes.

- 42% of new homes purchased were purchased by buyers looking to avoid renovations and/or repairs of plumbing and electrical.

- 31% of buyers buying previously owned homes did so because they considered it a better value.

- When deciding on a home to purchase, buyers in 2024 showed some compromises on their home characteristics.

- The most common compromise made was the price of the home at 30%, and the condition of the home at 23%.

- 31% of buyers said that they did not have to make compromises when purchasing their home.

Media age of a repeat buyers increased to 61 years old. Among all buyers the media age increased from 56 to 49 years old from last year. Median first-time buyer age increased to 38 years old from 35 last year. These ages are all record highs!

Key Takeaway

The real estate purchasing power is in the hands of Gen X and above. We need to market accordingly. Traditional media is still a focus of marketing campaigns – but needs to be highly targeted!

- 73% of recent buyers did not have a child under 18 in their home – the highest share ever recorded.

- 27% of all buyers have children under the age of 18 living at home, a historic low. This is down 30% from last year – but down from 58% in 1985.

- In 2024 12% of home buyers had one child, 10% had 2 children, and 5% had three or more children.

- Factors influencing neighborhood choice show highs of 59% for the quality of the neighborhood, but only 16% for the quality of the school district – a data point seemingly driven by the above factors.

Key Takeaway

Nationwide trends point to the fact that traditional young families with +2.5 kids are not driving sales in the current real estate market. This is especially true for areas like Daniel Island that see many 2nd home purchasers, buyers above the median purchasing age (57 yo), and buyers moving from high-tax more heavily urban states.

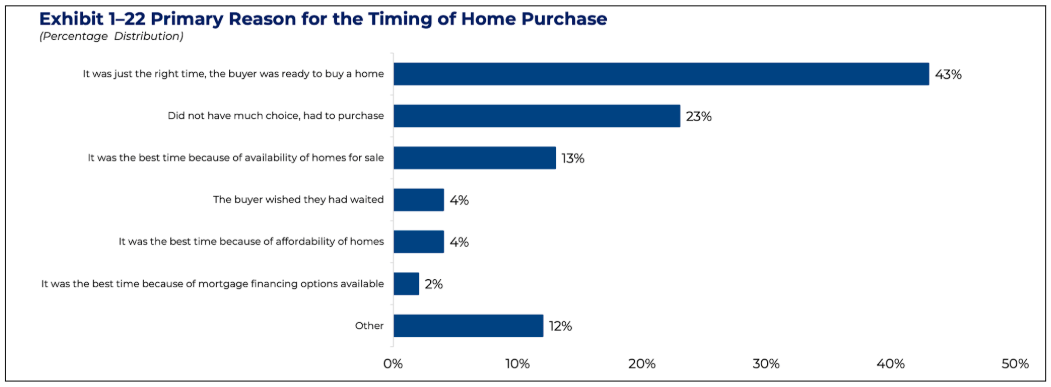

- 43% of all buyers said the timing was right and they were ready to purchase a home. 23% said they did not have much choice regarding timing followed by the fact that it was the best time because of home availability.

- In total 66% of buyers bought without being impacted by market factors.

- Only 4% said the timing was due to the affordability of homes and only 2% purchased due to mortgage financing options.

Key Takeaway

While a lot of focus is on mortgage rates and inventory as a key driver for home buying – the timing of 2/3 of purchases is not influenced by these factors. Sometimes timing is everything.

2024 Sellers

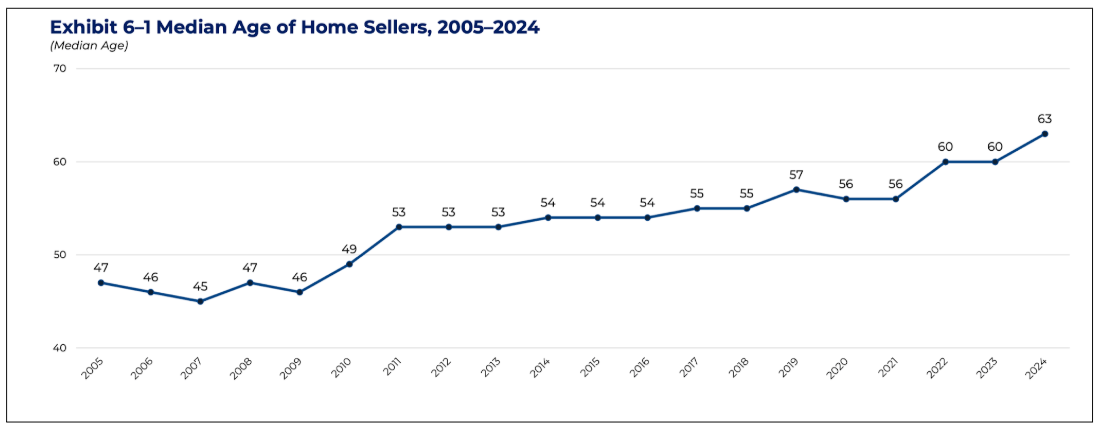

- The typical age of home sellers was 63 years old in 2024 and is the highest ever recorded.

- Of all homes sold on the market, 77% did not have children under the age of 18 residing in the home.

- For recently sold homes, the final sales price was a median of 100% of the final listing price – showing that a significant amount of sales prices were above full ask. This continues to be the highest recorded median since 2002.

- 90% of sellers sold with the assistance of a real estate agent, and only 6% were FSBO sales, an all-time low.

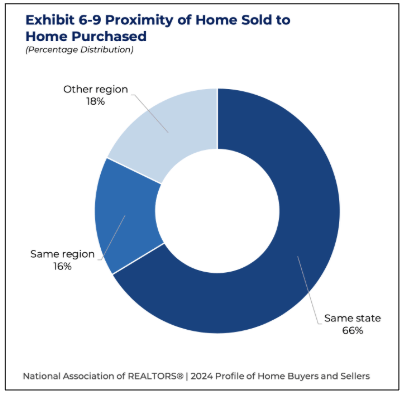

- 18% of home sellers purchased a home in another region to the one they sold a home. 66% of home sellers moved within the same state, and 16% remained in the same region.

- The median number of years a seller owned their home was 10 years, the same as last year. That number was higher than reported from 2000 to 2008, when the tenure in the home was only six years.

- Sellers placed a priority on three things in the home selling process – marketing the home to potential buyers, pricing the home competitively, and selling home within a specific timeframe.

The typical age of home sellers was 63 in 2024 – up from 60 last year and the highest recorded. In 2005 the typical home seller was 47.

Key Takeaway

Nationwide media age of home sellers at 63yo driven in part of average time of owning a property increasing to 10 years. Age would be higher on DI Parkside – even though average length of home ownership is closer to 5 years.

Home sellers in 2024 reported purchasing home in another region 18% of the time. 66% of sellers purchased within the same state, and 16% remained in the same region.

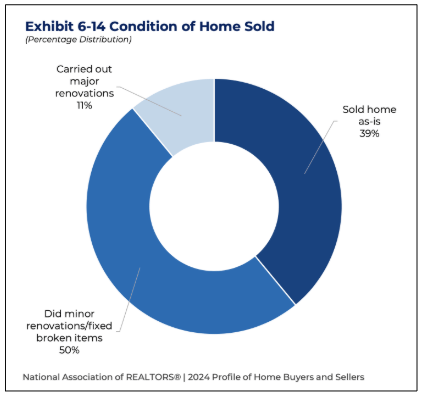

50% of home sellers said they did minor renovations or fixed broken items before selling. 39% of the home sellers reported selling their home “as-is.”

Key Takeaways

Moves outside of region have slowed since the immediate years after COVID as in-person “back to work” initiatives have expanded. Sales of homes in 2024 show that most sellers thought it was more important to get the home to market than do significant renovations. In a seller’s market this strategy proved effective based on seller’s feedback.

2025 What to Watch for Next

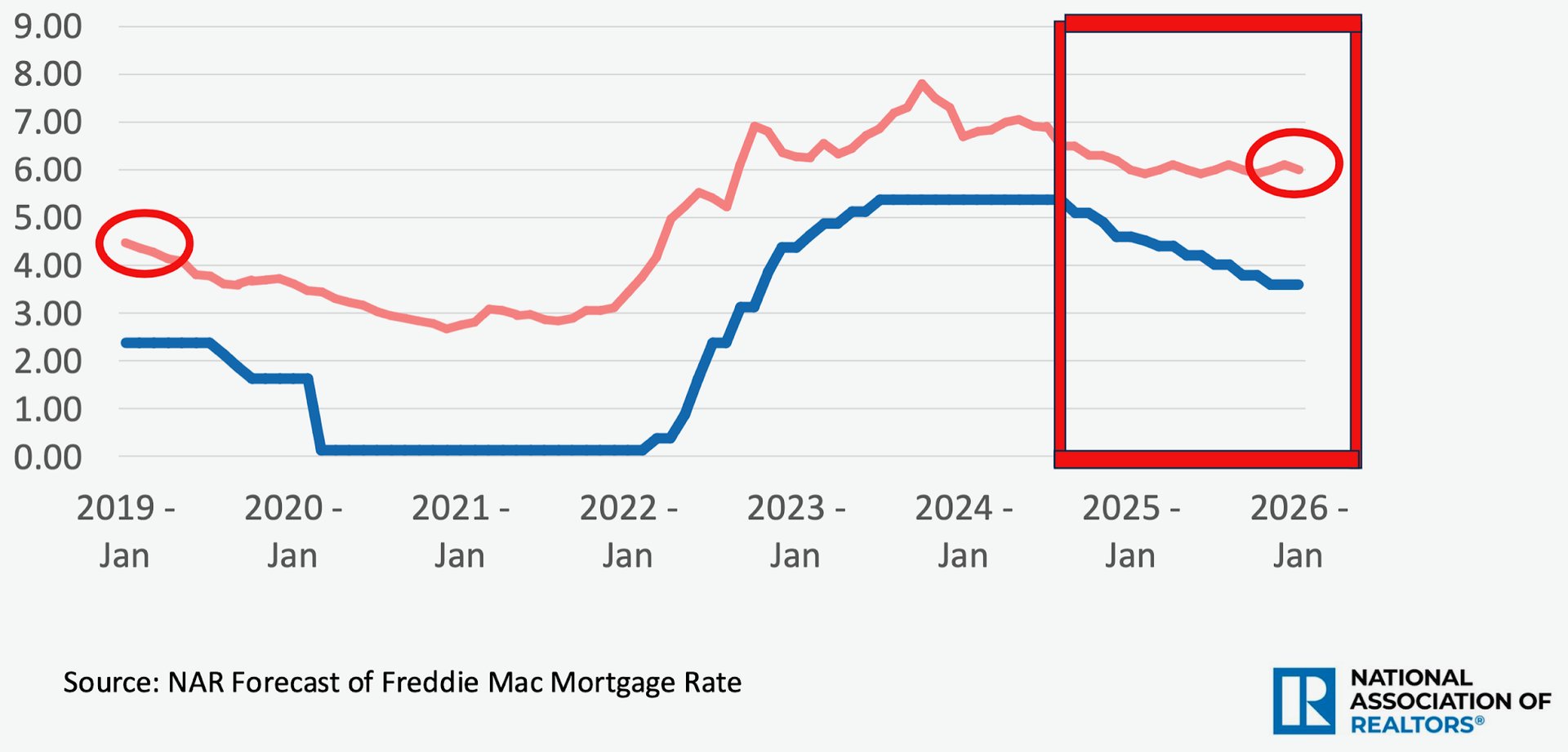

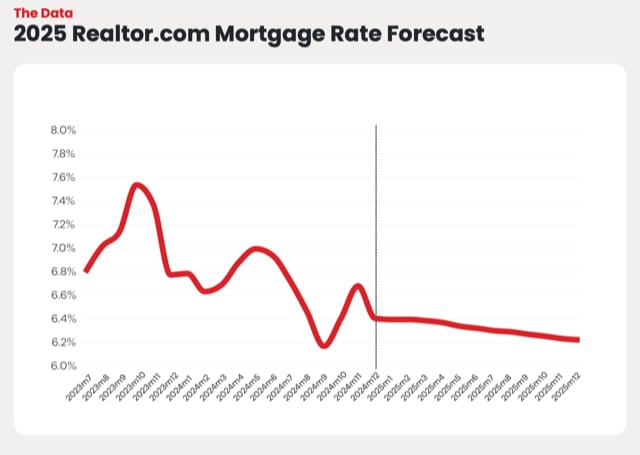

- Fannie Mae economists are predicting rates on 30 year fixed-rate mortgages will be closer to 7% at end of this year and remain above 6% in 2025 and 2026.

- Mortgage Bankers Association economists believe in a similar path – predicting rates will still be at 6.4% at the end of 2025 and 6.3% end of 2026.

- The total number of home sales are forecast to grow +4.6% in 2025 from 2024 (Fannie Mae).

- Volatility in real estate market forecasts due to general heightened fiscal policy uncertainty.

- Realtor.com economists expect home prices to continue to rise in 2025, although at a slightly lower pace of 3.7% nationwide. Besides rate decreases many economists are also expecting existing for-sale inventory to be +11.7% higher in 2025 than in 2024.

- Downward pressure on price growth due to increased inventory will slightly win out over the upward pressure on price growth due to falling mortgage rates next year for most of the US. US Median Sales Price Increase forecast to increase +3.7% (Realtor.com)

- In Charleston – and specifically DI – the continued and significant demand to move here creates pressure that should increase median sales prices by close to +7% through 2025 (Realtor.com)

Expect 6-8 rounds of cut to Fed Funds Rate 2024-2026 but the Mortgage Rate may not fall that quickly due to other factors in the economy

Key Takeaway

Total national home sales depend mainly on jobs and mortgage rates. Both factors can be impacted by financial policies. Many experts believe that if mortgage rates move below 5% it could lead to a median sales price increase of +10%. DI real estate market seems to be less dependent upon these factors due to high demand, affluent buyers, cash deals, high stock market, 2nd homes.

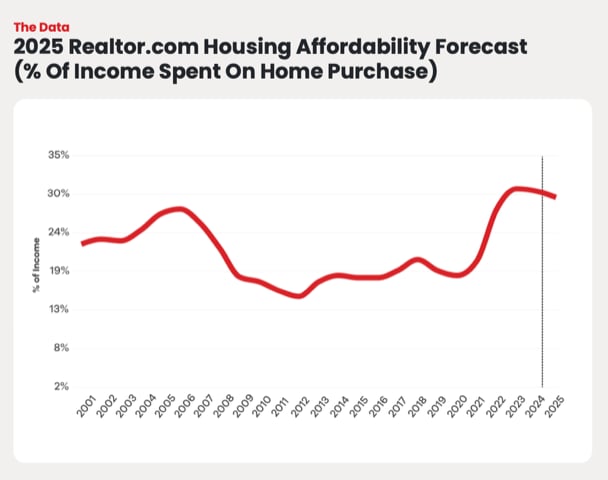

Mortgage Rates are expected to decrease slightly in 2025, but affordability will continue to be a significant issue in the housing market

Key Takeaway

30% of Household income spent on Home Purchase in 2024 is significantly higher than 2007-2020. Mortgage rate decreases should alleviate some of this issue. But the fact remains that the DI market – and the rest of the luxury market in Charleston – is not dependent upon mortgage financing due to high percentage of all-cash deals, older more affluent demographic, 2nd home purchases, and relocations from urban centers.

Two Competing Dynamics Impacting Inventory – “Locked in Effect” versus “Seller Timing”

Delayed Sellers Cannot Wait Longer Locked-in effect to be less strong over time. 10% of the US Market has a life-changing event happen per year that can prompt a move:

- 3.5 million new-born babies a year

- 1.5 million marriages, 700,000 divorces

- 3.5 million turn 65 years old

- 2 million deaths

- 25 million job switches

Key Takeaway

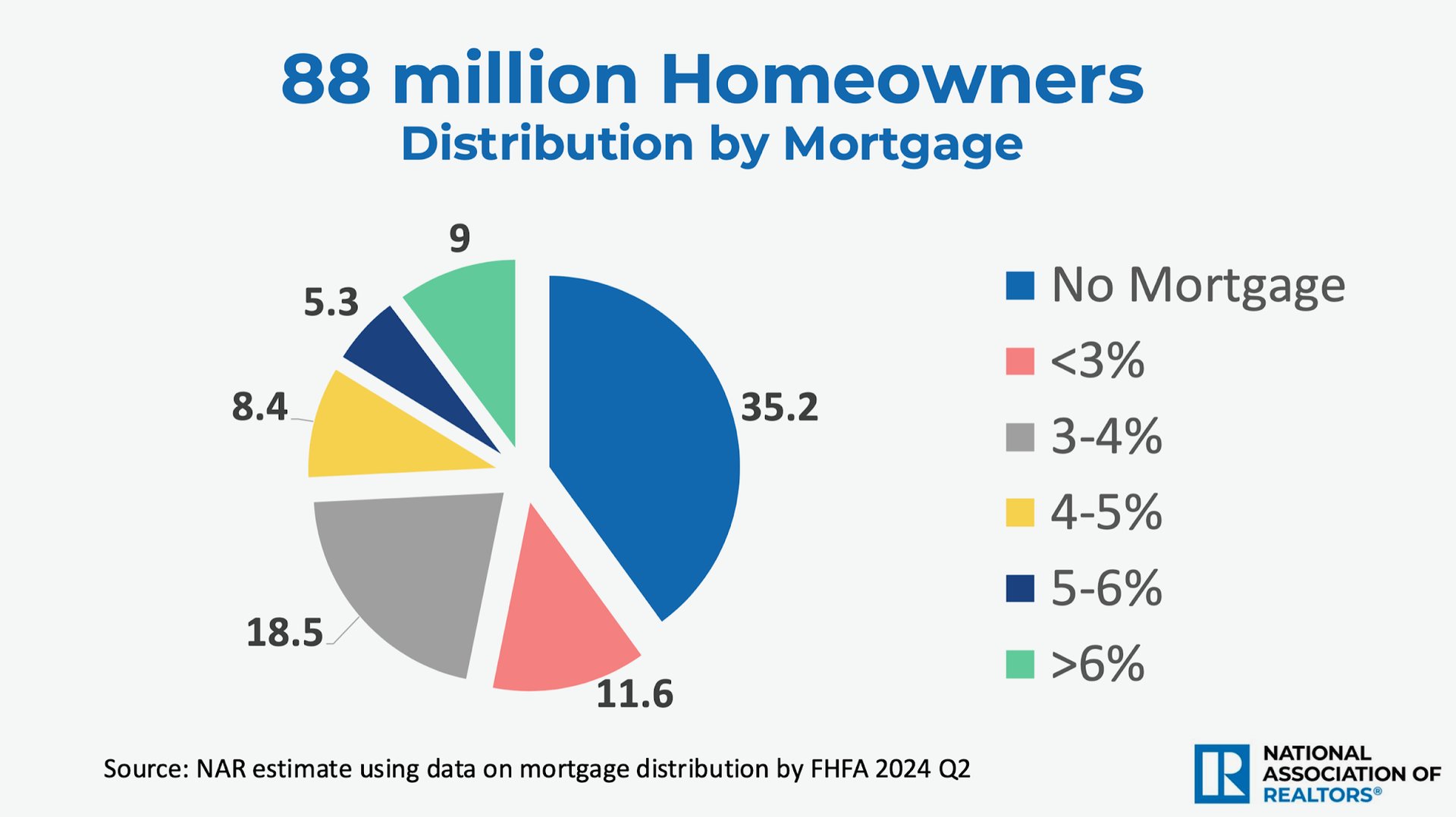

When we look at the real estate market it can be easy to assume that every homeowner will wait to sell at the optimal time in the market – and in an environment where selling your home could lead you to trade a sub-3% mortgage for a 6.8% mortgage why would they ever sell? Afterall, nearly 74% of homeowners have a mortgage rate 5% or less (including no mortgage)! Eventually though, life catches up with homeowners and nearly everyone choses to sell for one reason or another. This is the difference between investments in your home and investments in equities. Many sellers have delayed for years waiting for the right time related to mortgage rates – and this could cause a surplus of inventory in the market when mortgage rates are reduced below 5%.

2025 Key Take-Aways

- If you are considering selling now is a GREAT time to do so!! Factors are in play that may impact the extremely low housing inventory levels we have seen in 2024 – so you could have more competition later in 2025. National inventory could go up by as much as 11.7% - and the luxury level is more dependent upon competition than interest rates! (Fannie Mae)

- Experts predict a +2 to 3% increase in Charleston property values in 2025 – but as much a +7% median sales price increase for Daniel Island. Remember to speak with your agent about the micro-market in your area of Charleston (Realtor.com).

- Luxury Home sales are still driven by Cash buyers – as 40% of these purchases are all cash deals. Waiting on mortgage rates to drop will not help much here.

- Buyers should not be deterred to buy in this market if they find the perfect home – prices could be higher in 2025 as there will be more competition and there is always the opportunity to refinance or take an adjustable-rate mortgage if you believe mortgage rates will drop.

- When thinking of the long-term strength of the Charleston Real Estate market please note that the population of the Southeast is forecast to grow by 25% in the next 10 years. Charleston is positioned to remain a regional hub of business and tourism – as well as a leading target for those looking to relocate to a business-friendly, low-tax environment.

- While there are many factors to consider when deciding whether to begin the process of buying or selling a home in Charleston, please know that our buyer and seller strategies are designed to “win” in the current market.

- For sellers – we market lifestyle branding and cutting-edge demographic targeting for our homes to appeal to “affluent relocators.” We believe in developing bespoke marketing campaigns for each home we list, run national advertising campaigns along with local outreach, stage our homes to maximize their appeal, and drive affluent buyers to your door.

- For our buyers we utilize our unparalleled experience in the market to find off-market properties before they hit the market, employ cutting edge market research to help you make the best financial decisions, negotiate the best deal for you, and provide time-tested white-glove service every step of the way through your transaction.